At the end of November or beginning of December each year, car owners across the country receive notices about the need to pay vehicle tax. Legal entities and individual entrepreneurs independently calculate the amount to be transferred to the budget. And for individuals, the tax office makes the calculations. Inspectorate employees calculate the exact amount of transport tax based on the car model, year of manufacture, power and other conditions. However, not always all the necessary information is received by the Federal Tax Service on time. Therefore, errors are inevitable in some situations, and transport tax may need to be recalculated.

In what cases is transport tax recalculated?

- The car has been sold. Most likely, the data has not yet been received by the tax office, or has not reached the required department. You must inform the inspector about this and present the purchase/sale agreement.

- The car was stolen. In this case, the owner must provide a copy of the theft certificate received from the police. This can be done before the receipt for payment arrives. Then recalculation can be avoided.

- An individual owns several cars, but tax is assessed on only one.

- The tax was calculated incorrectly. The human factor is present in the tax office to the same extent as in other organizations. If, after receiving a receipt for payment of transport tax, you notice that the wrong brand of car or the wrong power is indicated in the calculations, you need to contact the tax office as soon as possible for recalculation.

- No benefit applied. In this case, you also need to write an application for recalculation, indicating the reason for the right to a benefit.

New rules for recalculating land tax and property tax from 01/01/2019

Recalculation of land tax for three years Quietly and without resonance, the Duma adopted Federal Law No. 334-FZ of August 3, 2018 “On Amendments to Article 52 of Part One and Part Two of the Tax Code of the Russian Federation.” Which in narrow circles was called the “budget killer.” In this article we will understand what this law ultimately provides? And is the adopted law so dangerous for the budget?

The law described above introduced serious amendments to the Tax Code of the Russian Federation in terms of changing the procedure for determining the tax base for property tax and land tax.

Specifically, the law includes a paragraph according to which, in the event of a change in the cadastral value of a taxable object based on the establishment of its market value by a decision of the commission for the consideration of disputes about the results of determining the cadastral value or a court decision, information about the cadastral value established by the decision of the said commission or a court decision, entered into the Unified State Register of Real Estate are taken into account when determining the tax base starting from the date of commencement of application for taxation purposes of the cadastral value that is the subject of a challenge.

A similar paragraph has been introduced not only in relation to land plots, but also in relation to capital construction projects (CCF), which also include administrative and business centers and shopping centers (complexes) and premises in them, non-residential premises, real estate objects of foreign organizations , residential buildings and residential premises.

In addition, the law establishes the procedure for determining the tax base in the event of a market value being established in relation to a property by decision of a commission or a court decision, but also due to the correction of errors made in determining the cadastral value and changes in the qualitative and (or) quantitative characteristics of the object.

Recalculation of land tax for previous periods

The law also clarifies the list of persons entitled to benefits when paying property tax and land tax. The law establishes a list of property to which it applies.

The main part of the law is contained in its final part, according to which:

- the provisions of the law on tax recalculation apply to legal relations that arose from 01/01/2015 in relation to persons with disabilities since childhood and disabled children;

- owners of rooms, apartments, private houses, parking spaces and parts of these real estate objects can count on legal relations that arose from 01/01/2017;

- Land owners are the least fortunate. For them, the procedure for recalculating land tax for previous periods is subject to application to information on changes in cadastral value entered into the Unified State Register of Real Estate on grounds that arose from January 1, 2021.

That is, the norms of the last part are applicable only to new cadastral assessments, decisions on which will be made after the law comes into force. The law itself comes into force on January 1, 2021.

Recalculation of land tax when the cadastral value changes. Not for all periods, according to the provisions of the above law, it will be possible to recalculate the tax. The law sets a framework, limiting the possibility of a retrospective tax recalculation to three years from the date of sending a tax notice about the recalculation of land tax or property tax.

The above rule, on the one hand, is restraining, protecting to some extent the interests of the state. On the other hand, it is another loophole for delaying the process and delaying the moment of tax recalculation for government agencies and courts.

Retroactive recalculation of land tax I am asked: “Why didn’t the legislator make it possible to carry out a retrospective recalculation of existing court cases and state cadastral valuations in relation to land plots?” Answer: “The legislators simply did not want the law described above to become a “budget killer” for our country in the next tax period.”

And yes, the Government of the Russian Federation carried out the will of the President and dealt with the cadastral valuation, ensuring the protection and love of the people, while once again infringing on the interests of business.

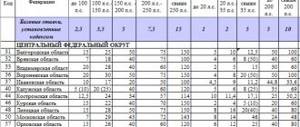

Recalculation of tax on a sold car

The transport tax calculation period is calculated in months. Therefore, in order to understand when it should stop accruing, you need to know the date of conclusion of the purchase/sale agreement.

If the sale was completed in the first half of the month before the 15th, then the tax will be charged to the new owner from this month. If the contract is dated in the second half of the month, then the current month will have to be paid to the former owner.

Thus, using the receipt you can check the correctness of the accrual after the sale.

Why might the calculation be wrong? The reason is simple. The tax office did not receive information from the traffic police. Or the employee who calculated the tax was inattentive.

What should the former owner do in this case? First of all, you need to contact the tax office to find out the reasons. Perhaps the mistake was made due to inattention and, in connection with the sale of the car, the inspector will correct it himself. If not, the individual needs to confirm the fact of selling the car by submitting a purchase/sale agreement.

- Take a certificate from the traffic police about your deregistration for a specific car;

- Contact the tax office at your place of registration;

- Fill out the application for recalculation;

- Attach a copy of the purchase/sale agreement to confirm the information provided.

You can fill out the application yourself and send it to the tax office by mail.

The situation will become more complicated if, after receiving ownership of the car, the new owner does not register the car in his name. Then you won’t be able to avoid unnecessary expenses on someone else’s tax.

Recalculation for a stolen car

Car theft causes a storm of negative emotions. Therefore, there is not the slightest desire to remember about the transport tax. However, when at the end of the year it becomes necessary to pay for a car that the owner has not used, you have to pull yourself together.

According to the Russian Tax Code, the owner of a car has the right not to pay tax during the theft. However, you still need to notify the tax office about this. To recalculate, the owner must contact the police and report the theft.

Traffic police officers will issue the owner with a certificate of theft and initiation of a criminal case. You must contact your local Federal Tax Service with these documents. There the motorist fills out an application.

Recalculation of transport tax in connection with the benefit

A certain category of citizens has the right not to pay vehicle tax. These include pensioners, large families, disabled people of groups 1 and 2, as well as heroes of Russia and the USSR. If the tax at the end of the year does not take into account the car owner’s right to a benefit, you need to contact the tax office with an application and documents confirming the legality of applying the benefit.

It is not necessary to use the benefit. That is why the tax office does not begin to apply it automatically.

To receive your legal deduction, the beneficiary must submit an application for a transport tax benefit and, if necessary, an application for recalculation for the last three years.

Owners of large trucks weighing more than 12 tons are required to pay tax according to Plato. It provides for tolls on federal highways. For such motorists, a tax benefit is also provided. If the calculation is incorrect, the owner has the right to recalculate the accrued tax.

How to write an application for transport tax benefits?

Application for tax recalculation

To the Federal Tax Service, Interdistrict Inspectorate of the Federal Tax Service of the Russian Federation No. __ for the _________ region Address: ___________________________________

Applicant: _____________________________ Address: ______________________________

STATEMENT

I, ______________________ ____________ born I am the owner of a land plot located at the address: ______________________ with cadastral number ________________. Recently, the Interdistrict Inspectorate of the Federal Tax Service of Russia No. ___ for the __________ region sent Tax Notice No. _______ to me, in which I was informed that I had been charged a tax amount of ________ rubles. ___ kop. Also, the notification indicated that as of __________, I had an arrears in the amount of ____________ rubles. ___ kop. and arrears of penalties in the amount of ________ rub. ___ kop. (Attached is a copy of the notice).

For information, I was informed that if I have the right to tax benefits, then in accordance with the legislation on taxes and fees, I need to present to the tax authority the documents that are the basis for the provision of tax benefits. In fulfillment of the above requirement, I provide the following information.

In accordance with Art. 387 of the Tax Code of the Russian Federation, land tax (hereinafter in this chapter - tax) is established by this Code and regulatory legal acts of representative bodies of municipal formations, is put into effect and ceases to be in force in accordance with this Code and regulatory legal acts of representative bodies of municipal formations and is obligatory for payment in the territories these municipalities. When establishing a tax, regulatory legal acts of representative bodies of municipalities (laws of federal cities of Moscow and St. Petersburg) may also establish tax benefits, grounds and procedure for their application, including establishing the amount of tax-free amounts for certain categories of taxpayers.

I, ______________, am a recipient of an old-age pension, a labor veteran, which is confirmed by the relevant certificates (I have attached copies of the certificates). So, since ____________ I have been assigned the second group of disability due to a general illness. My disability has been established for an indefinite period, and therefore I am incapacitated.

In accordance with Art. 391 of the Tax Code of the Russian Federation, if the land plot is owned, including by a person who is a disabled person of group II (if the disability was established before ___________), then the tax base from which the amount of tax is calculated is subject to reduction in the amount of ____________ rubles. ___ kop.

Also, in accordance with Art. 395 of the Tax Code of the Russian Federation, certain categories of taxpayers are provided with tax benefits (that is, they are exempt from paying land tax).

I believe that I, as a pensioner, a disabled person of the second group, have the right to receive the appropriate tax benefits established in the Tula region. Also, if I have the right to receive appropriate benefits, I ask you to return to me the overpaid amount of tax for the last three years. Please transfer the specified amount to my Sberbank account _________________________________.

Moreover, to resolve the issue of reducing the amount of tax collected from me, I had to resort to the help of lawyers, for whose services I paid _________ rubles. ___ kop. I also ask you to transfer the specified amount to the above account.

So, in accordance with Art. 2 of the Federal Law of the Russian Federation of May 2, 2006 “On the procedure for considering appeals from citizens of the Russian Federation,” citizens have the right to apply personally, as well as send individual and collective appeals to state bodies, local governments and officials.

Based on the aforesaid and guided by Article. 2 Federal Law “On the procedure for considering appeals from citizens of the Russian Federation”

ASK:

1. Recalculate the tax accrued to the Applicant in accordance with the benefits available to him; 2. Return the overpaid amount of tax to the Applicant by transferring it to the above account; 3. Please inform me about the decision made on this application in writing at the above address;

Appendix: 1. Copy of the Moskvich Social Card; 2. Copy of the Tax Notice; 3. A copy of a certificate of disability; 4. Copies of the pension certificate and the Veteran of Labor certificate; 5. A copy of the contract for the provision of legal services for a fee with copies of payment documents;

" "______________ G. ______________/_____________

How to submit an application for recalculation of fuel tax?

Taxpayers have the right to submit an application to the Federal Tax Service at the place of registration in person to the inspector, through an authorized representative with the provision of the original power of attorney, as well as through the Russian Post by sending a letter with a list of attachments. In addition to standard methods, the State Services service is gaining popularity. You can also submit an application through it if you have a verified account.

The application form can be found and obtained from the Federal Tax Service or found on our website. The Tax Code does not have an approved application form, so you can write it in free form.

Dear reader! Didn't receive an answer to your question? Our expert lawyers work for you. It's absolutely free!

- Moscow ext 152

- St. Petersburg ext 152

- All regions ext 132 (Toll free)

The samples differ in the reasons for requesting a recalculation, but in general they have the same structure.

- In the upper right corner it is necessary to write that the application is intended for the head of the tax office in which the individual is registered, and the full name, telephone number, address of the taxpayer;

- Next, indicate the name of the application, for example, “Application for recalculation of transport tax in connection with the theft of a car”;

- In the text, indicate a link to the article in the Tax Code of the Russian Federation and the reason why the individual is asking to recalculate the accrued amount;

- List the technical characteristics of the car (make, license plate, year of manufacture, power, etc.);

- Indicate the method of contacting the taxpayer. The tax office can send a response by mail or deliver it during a personal visit;

- List the attached documents confirming the legality of the recalculation;

- Signature and current date.

applications for recalculation of transport tax

How to write an application to the tax office for recalculation of transport tax

The application form for recalculation of the TN comes along with the tax notice. You will find it at the bottom of the same sheet where the car tax calculation is given.

So, if you see that the tax amount has been calculated incorrectly, cut the application form along the line and write your full name in the corresponding line. Remember that the tax office does not consider anonymous applications.

What to write next depends on the reason for recalculating transport tax for individuals:

1A TN was charged for the car you sold.

Check the box next to the line “Taxable objects do not belong to me” and indicate the make and license plate number of the car sold.

2TN was calculated incorrectly.

Check the box next to “The tax notice contains incorrect information.” Indicate in the table the section number, columns and lines with the error and write the correct value next to it.

For example, in our case, the tax amount was higher than expected, since it was calculated based on a tax base of 200 hp, although in fact the power of our car is 120 hp. In this case, a sample application to the tax office for recalculation of transport tax will look like this:

An error in the calculation could also occur due to an incorrectly indicated tax rate (column 6), the number of months of car ownership (7) or the amount of benefits (8). In this case, proceed in the same way - indicate the column and line where the information does not correspond to reality and write the correct value next to it.

3ТН was not charged to one of the cars.

If you bought another car in 2021, but the tax on it was not calculated in the 2021 notification, you should definitely report this. To do this, check the box next to the line “The tax notice contains no information...” and indicate the make and license plate number of the car that was not calculated for you.

Once the details of the error are indicated, write your email address (if you have one) and phone number. Next, put the date and signature. With this, the statement is ready.

Important!

You can attach to your application copies of documents that confirm the need for recalculation (for example, a copy of the vehicle title to prove the number of horsepower), but this is not at all necessary. In any case, the tax office itself will contact the traffic police for the necessary information.

What documents need to be attached to the application?

When submitting in person or sending by mail, the car owner who is counting on recalculation of the technical tax must attach the following documents to the application.

- Passport of a citizen of the Russian Federation (or other identification document);

- TIN, if any;

- Documents confirming ownership (PTS);

Copies of these documents are attached to the application, regardless of the reason for the recalculation.

In addition to them, the inspector may request supporting documents upon admission. These include:

- Purchase/sale agreement and document on deregistration of the car from the traffic police;

- Certificate of car theft;

- PTS or other document confirming technical characteristics;

- A document allowing the benefit to be applied.

The most convenient way is to come to the tax office with the specified documents and fill out an application for recalculation on the spot, since most inspectors require you to provide original documents.

During what period is it possible to recalculate TN for individuals?

Usually, owners quickly discover the error and recalculate for the previous year. However, this does not always happen. Tax officials have the right to recalculate incorrectly calculated tax for the last three years. However, they cannot do this without a written statement from the owner of the car. Thus, if an error was discovered in 2021, recalculation can be made for 2021, 2021 and 2021.

After recalculation, the applicant can offset the overpayment against future payments or refund the money. The owner must indicate this in the application for refund of the overpaid tax. It indicates the recipient's bank details.

Can the Federal Tax Service recalculate the technical tax on its own?

The situation when a motorist did not submit an application to the tax office, but a new receipt with an adjustment arrived, occurs quite often. Usually in such cases there is an increase in the amount payable.

Additional charges have to be made for the same reasons as recalculation: inattention of tax officials who indicated less power than needed, information that was received at the wrong time, and so on.

Despite the indignation of car owners, the Federal Tax Service has the right to do this in accordance with Articles 31 and 32 of the Tax Code of the Russian Federation. The taxpayer, in case of disagreement with the additional assessment, may contact the tax office to clarify the circumstances. If there is no result, you can fight for your innocence in court.

Tax payments of the car owner are his direct responsibility to the state. Money received by the budget as a transport tax is spent on building new roads and repairing old ones. However, there is no such thing as extra money. And paying additional tax amounts is expensive. Therefore, the car owner must independently control the tax accrued on the receipt. If it is necessary to submit applications for recalculation, the motorist needs to collect supporting documents and submit the originals to the Federal Tax Service at the place of registration. After considering the issue, you need to write an application for a refund or offset in favor of future payments. The main thing is not to delay in correcting tax mistakes. After all, the period for which recalculation is possible is only 3 years.

What to do if property tax was calculated incorrectly for the previous year?

If the property tax was calculated incorrectly, which you became convinced of after checking all the data and using electronic services, you need to prepare an appeal.

If the reason is an incorrect cadastral value, then the appeal is sent to the commission for resolving disputes regarding cadastral value or directly to the regional court.

If this is not the reason or your claim was satisfied with the recognition of an error in the Unified State Register of Real Estate, then further actions depend on whether the amount on the “wrong” receipt has been paid or not yet. For example, the notification was sent to you several months before the payment deadline - then you need to file a claim for recalculation of the property tax for individuals.

If you paid by receipt, then this involves not only filing an application for recalculation, but also submitting an application for a refund or offset of overpaid property tax for individuals.